As a management consultant, I’m often contacted by entrepreneurs seeking my help to develop great go-to-market and growth strategies before they have even confirmed if their idea is something customers would be willing to pay for. This risky approach is something that many startups were able to get away with during the age of blitzscaling and growth at all costs, a time when venture capital (VC) firms were flush with cash and willing to take chances on companies that hadn’t even validated their core offering’s product-market fit. However, those days are over.

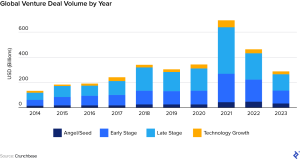

Despite the burst of interest in AI-themed startups, VC funding in 2023 was at its lowest level since 2018. Investors are growing more selective, and many founders are having to do more with less. That means scrappy entrepreneurs are turning to bootstrapping to get their businesses off the ground, or they are recognizing that their business ideas simply aren’t ideal candidates for VC funding, making bootstrapping the best choice.

By going it alone, founders have to be disciplined from the very beginning because it’s their own money on the line. A solo approach forces entrepreneurs to manage costs religiously and focus on sustainable organic growth, sometimes forgoing inorganic expansion opportunities that VC-funded startups would not think twice about seizing.

But if bootstrapping requires more financial discipline, it also offers founders more freedom. Without investors to appease, these founders can first make sure that their product or service actually solves a problem that a large enough number of customers are willing to pay to solve. No one can afford to become the next Juicero, which failed in large part because customers realized they didn’t need a $400 Wi-Fi-connected device to squeeze juice packets that could just as easily be squeezed by hand.

Instead of growth at all costs, the lesson new entrepreneurs should embrace is good old-fashioned validated learning to refine their core offering and achieve product-market fit.

You don’t need an elaborate go-to-market plan to do that. You don’t need VC funding. You just need to start. In this article, I show you how.

Develop Your Core Offering

Every new business starts with a leap of faith—an educated guess, essentially—that the product or service fills a need in the marketplace. But the next step should be to put some data behind that faith, and make sure your core offering has traction and the right unit economics before you do anything else.

I once worked with an entrepreneur who wanted to help the development teams of large marketing agencies build visually consistent and coherent multipage websites. He had often been hired to create these as a freelancer, and he knew from direct experience that this was a problem that needed solving in this niche.

When I first met him, his priority was building out a five-year plan—but he hadn’t really figured out exactly what he was selling yet, or to whom. He was still trying to decide between a project-based business model, a subscription-based service for access to a specialized WordPress plugin for agency use, or a combination of the two. Nor had he worked out who his customer might be within the agency, much less how to craft his offer to appeal to them.

Clearly, my client (or any entrepreneur at this stage) wasn’t ready for any kind of long-term plan. Instead, I used Alex Hormozi’s $100 Million Offer framework to help him work out exactly what his core offering would be. There are many ways to determine a core offering; Hormozi’s approach is to maximize the perceived value of your core offering in the eyes of your clients by identifying their dream outcome and guaranteeing the likelihood of achieving it while minimizing the time and effort it requires. I like this approach because of its simplicity: People are willing to pay a great deal for a solution that solves their exact problem efficiently and effectively, and this framework puts those needs front and center, making it easy for you to differentiate your product or service.

Using this framework, I collaborated with my client to list:

- The problems he wanted to solve.

- All the obstacles the customer might face along the way.

- How those obstacles could become solutions.

- How he could provide those solutions.

We then eliminated any offerings that would be too difficult or expensive to fulfill or too difficult to sell.

Test, Learn, Refine

I usually recommend that entrepreneurs start by building out a minimum viable product (MVP)—a concept that should be familiar to anyone who’s spent time in tech circles. This is a cheap, low-effort (but still appealing and functional) version of your product that’s designed to test the effectiveness of your idea. Even if you already have a good notion of what you think your final product might look like, this isn’t the time to build it out entirely because you might discover that your customers actually want something a little—or a lot—different.

Instead, zero in on the central solution your product or service would provide and build out an offering as quickly and as inexpensively as you can. If taken to the extreme, AppSumo founder Noah Kagan says, you shouldn’t spend money to validate an idea, and you don’t need to know how to code. Instead, you should seek out a no-code or low-code solution. For example, if your product is a short-term apartment exchange service, you don’t need to build out an app and test it right out of the gate. Perhaps you create a Facebook group or Skool community instead, or even just a shared spreadsheet that you promote over social media. Then you manually match potential users and put them in touch with each other.